These are extreme and volatile times for the energy markets. There are no sure-fire rules for choosing when to sign up to PPAs but awareness is essential. Welcome to the second monthly market summary, produced in partnership with The Greenspan Agency.

As we head into the winter, The weather will be a key market driver in the coming months; likely to impact both gas demand and renewable supply. Markets rose significantly from 1st September to 5th September, but then dropped thereafter. The overall result is a decrease of -14% for Winter22 and a marginal change of -1% for Summer23 from month start to month end. Below summarises the key market drivers this month.

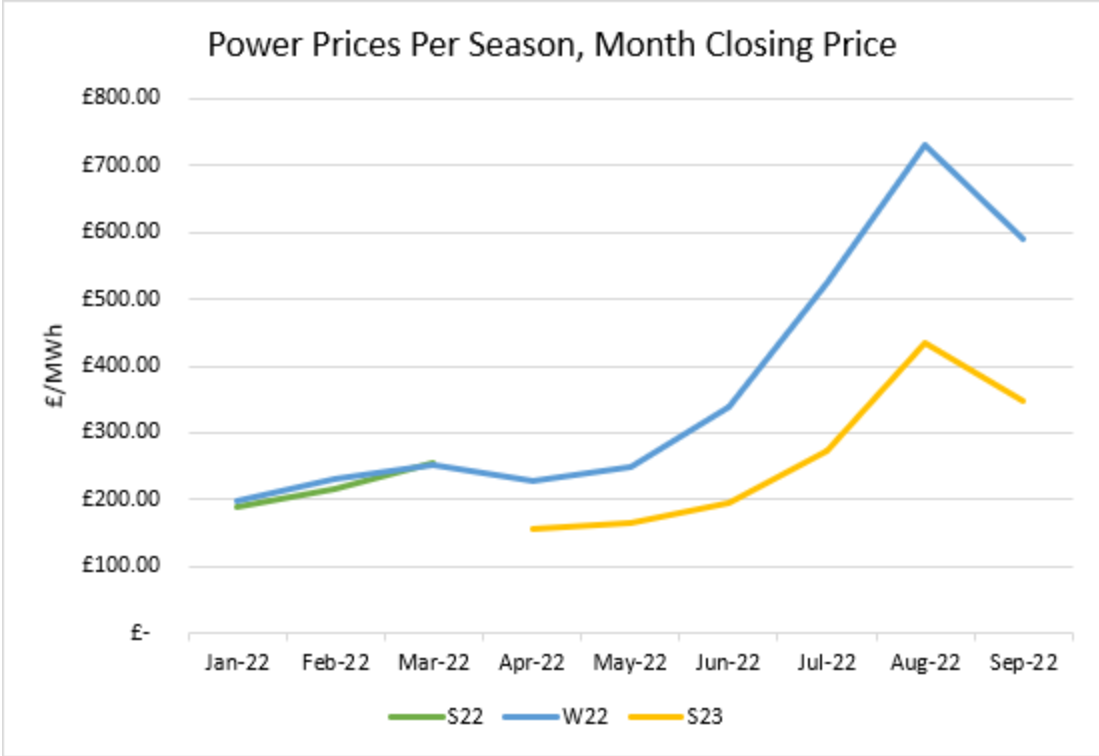

As has been the theme of the last few years, significant global developments influenced both the power and gas markets this month. The overall picture is one of high volatility and uncertainty, with the market seemingly reacting to the news cycle by the hour. The war in Ukraine continues to dominate the wholesale market, with the EU and Russia at loggerheads about commodity price caps and delivery volumes. Yet Winter22 power prices showed a steady drop from month start to month end (see graph and table below).

The end of August saw the EU announce that they would be intervening in the energy commodity market, by capping the price of Russian fossil fuels. At the time, the detail was yet to be confirmed. Following this news, Russia refused to reinstate flows through Nordstream 1, citing turbine malfunctions and leaks. The pipeline has remained offline since, last exporting on September 2nd. Power prices shot up by 25% as a result, with Winter 22 peaking at £717/MWh on the 5th of September. Prices remained high as Putin threatened to cut off all commodity supply to Europe. On September 15th, the EU announced their market interventions would be limited to Russian crude oil. With gas market caps lacking, the market calmed.

However, the second half of the month largely saw wind increases above seasonal norms, depressing prices. On the 16th of September, energy generation in the UK was high enough that power was exported to France. Gas and power prices continued to drop as Norwegian gas flows returned and numerous cargoes of LNG supplies arrived on the UK shores. These drops were seen despite escalations in the Russian-Ukraine war.

The final week of September saw extreme volatility, with cold weather hitting the UK. By September 28th, reports of several extensive gas leaks along the Nordstream 1 and 2 pipelines shocked the market. Swedish and Danish authorities reported that the leaks were a result of Russian sabotage. Whilst this caused prices to rise by as much as 14%, Winter 22 and Summer 23 pricing remained below the peaks of September 05th and late August.

Closer to home, the new Chancellor of the Exchequer announced the UK ‘mini-budget’ on Friday the 23rd of September, which led to a severe drop in the strength of the Pound against the US Dollar and the Euro. It is difficult, given the numerous global factors discussed above, to quantify the significance the falling pound has had on market movement.

|

Closing Price, Last WD of Sep-22 |

Overall change through Sep-22 |

||

|

Win 22 |

Sum 23 |

Win 22 |

Sum 23 |

|

£590.00 |

£347.00 |

-14% |

-1% |

The Greenspan Agency produce the report on a best endeavours basis and has been supplied for your interest; the facts in this report are for background information and should not be relied upon exclusively for decision making.

If you have any queries about the content in this report, please contact amy@greenspanenergy.com or lara@greenspanenergy.com.

Contact Us

Send us a message

or enquiry

"*" indicates required fields