The first few days of February saw some minor price increases as weather fundamentals (predicted cold snaps coupled with low wind) added pressure to the gas market. Carbon pricing increased as renewable output was hindered. These increases were short lived, and the downward trend returned in the second week of the month.

Wind output increased in the second week of the month – leading to falling gas, carbon, and power pricing. Power pricing continued to decrease from the second week as power and gas demand remained lower than seasonal norms.

Concerns over LNG supply fed into the market mid-month; despite healthy supply, the market remains anxious over decreasing price spreads between European and Asian markets. By month end, the weather in Asia remained mild, supporting European LNG supply.

Market movement in the last week of February was indicative recent trends: Price increases of £2/MWh were seen on 23rd and 24th February. However, these were swiftly lost on 27th Feb, where decreases of £6/MWh were seen. Decreases continued as February came to a close.

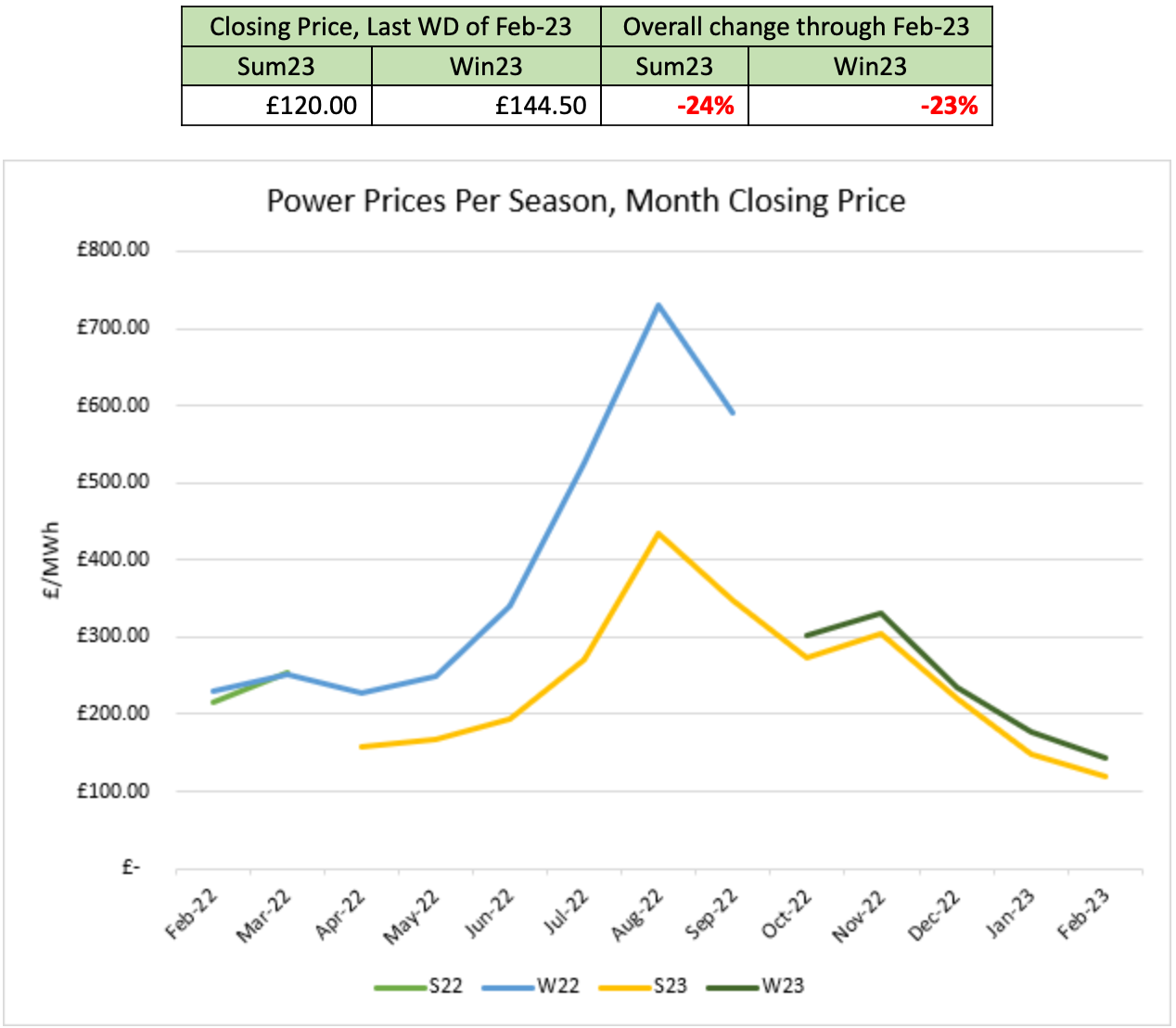

Overall, February demand was 8% lower than typical figures; this is partly due to decreased domestic usage. Winter23 pricing is at its lowest since April 2022.

The Greenspan Agency produce the report on a best endeavours basis and has been supplied for your interest; the facts in this report are for background information and should not be relied upon exclusively for decision making.

If you have any queries about the content in this report, please contact amy@greenspanenergy.com or lara@greenspanenergy.com.