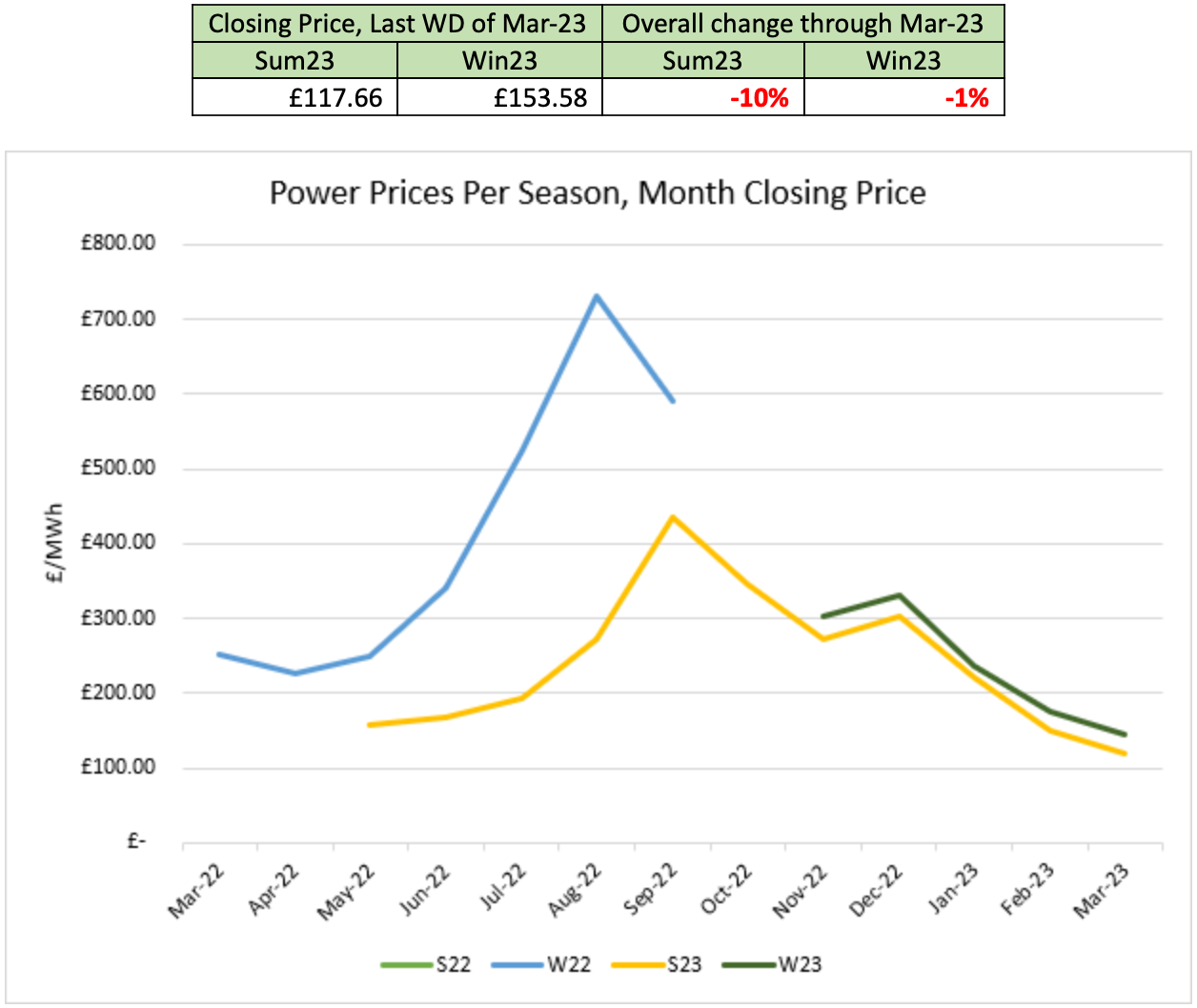

The end of this month marked end of the “winter season”. Whilst, overall, March saw further decreases in the market, risk remains for the upcoming winter (Winter23). The first half of the month saw decreases in line with January and February. However, the trend shifted with the cold weather and international pressures mid-month. The political uncertainty in France, and resulting energy strikes, added uncertainty and price rises in both the Summer23 and Winter23 season. Overall, there was a 23% decrease in Summer23 pricing, but very little difference in Winter23 pricing, suggesting unpredictability for the upcoming winter season.

Despite the cold weather at the start of the month, both gas and power prices moved downwards as supply remained strong. This was further impacted by reduced domestic activity in the current economic climate.

The weather took a turn around March 07th, resulting in several coal powered stations running to meet demand. Record power prices were paid out to gas generators to ensure supply on the evening of the 07th.

Gas prices decreased as the weather improved, however power prices remained high on March 09th as it was announced that cracks had been found in the Penaly 1 reactor; casting doubts over the expected return to service in May. In turn, fears of increased interconnector exports to France led to prices rises and increased volatility through to the 14th. Carbon pricing also increased in this period, uplifting power pricing.

On March 17th, Norway announced that the proposed interconnector to Scotland (NorthConnect) would not go ahead; this is to protect Norway’s domestic power supply. This caused an increase in prices in the farther term. Coincidentally, this occurred at the same time as increased Norwegian imports to the UK energy system, which caused near term gas and power prices to drop.

Price rises were short lived as strong LNG and mild temperatures pressured gas, and subsequently power prices. The resolution of the French industrial disputes and increasing confidence in European hydro reserves following promising rainfall predictions depressed prices.

The market remained volatile in the final two weeks of the month; LNG cargoes remained strong, depressing pricing, however uncertainty over French nuclear availability and cold weather forecasts periodically pushed pricing up. Largely, the market remains unsettled and unpredictable. Pricing remains intertwined with LNG supply and weather fundamentals. The outlook for the upcoming year is uncertain in a market impacted by Russian sanctions.

The Greenspan Agency produce the report on a best endeavours basis and has been supplied for your interest; the facts in this report are for background information and should not be relied upon exclusively for decision making.

If you have any queries about the content in this report, please contact amy@greenspanenergy.com or lara@greenspanenergy.com.

Contact Us

Send us a message

or enquiry

"*" indicates required fields