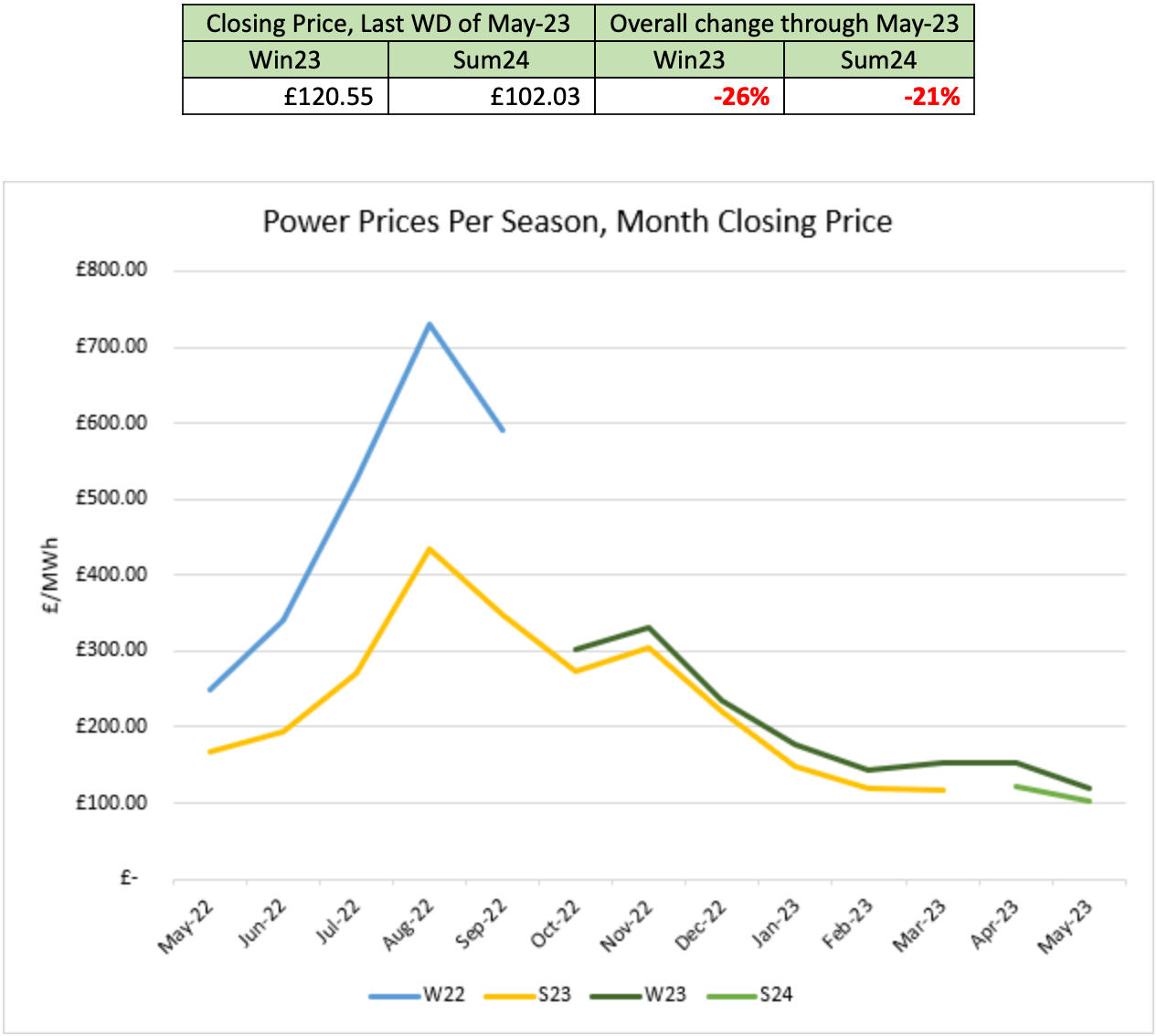

The long-awaited summer has arrived in the UK and the (highly anticipated) sunshine resulted in solar output being 20% over the seasonal average this month. This balanced any upward market pressure from low wind. Whilst the Norwegian gas field outages did result in market increases, these were temporary, and the overall picture was one of consistent decreases. French nuclear availability remains a key volatility influencer; recent reports suggest that output will be on the rise as we approach winter, despite European figures as a whole decreasing. European gas storage is already at a healthy 60% full this month, showing a good outlook for the future season.

The start of the month saw consistent decreases in both gas and power; gas (i.e., LNG) supply remained healthy and buoyant against the seasonal drop in demand. Norwegian gas outages on May 09th-10th resulted in minor market increases in the front market but these were temporary.

The gas system remained oversupplied. Throughout the first half of the month prices decreased following the news on the upcoming increase in French nuclear output. News on the repair of stress fractures in the fleet gave confidence to the nuclear availability in the coming winter.

Carbon prices rose for most of the first half of the month, but these failed to feed into power price increases until May 18th. Again, the rises were soon wiped from the market amidst healthy gas and renewable output.

Towards the end of the month, power and gas prices diverged. Gas prices rose following continued Norwegian outages, but power prices decreased in response to the sky-high solar output, which was 20% above seasonal norms. The end of the month saw gas prices subsequently decrease with the drop in fuel fired generation and heating demand given the warm weather.

Much apprehension remains for the future of power prices in the upcoming winter. However, gas storage remains healthy as at the start of summer; and it seems likely that stocks will be refilled by the close of the season. Whilst the EU estimates that gas cuts will be greater than all Russian imports for 2023, much of the future LNG supply has been contracted out. Future market stability seems possible, but not guaranteed.

The Greenspan Agency produce the report on a best endeavours basis and has been supplied for your interest; the facts in this report are for background information and should not be relied upon exclusively for decision making.

If you have any queries about the content in this report, please contact amy@greenspanenergy.com or lara@greenspanenergy.com.

Contact Us

Send us a message

or enquiry

"*" indicates required fields