September seemed to be a story of two halves for weather fronts, but a consistent trend on falling prices. The beginning of September saw summer finally arrive with warm weather covering the continent. It was the first time the UK had seen temperatures above 30 degrees Celsius for 7 consecutive days during this month. This brought solar generation up to 20% above seasonal norms compared with wind, which did not perform against seasonal averages.

There were threats of Chevron industrial action in Australia which pushed gas pricing upwards but this was heavily offset by UK gas storage being at 88% capacity by 1st September and European gas storage being above 90%, which supressed it further.

The latter half of September brought stormy conditions as we saw wind perform 20%+ above seasonal norms and 15.5 GWh of volume produced from wind on 19th September (Circa 50% of UK demand). As a result of continued high windspeeds, Day Ahead contracts reached their lowest since March 2021.

During the third week in September, renewables accounted for 49% of GB energy mix; a fantastic result before we entered the winter season.

The announcement from the Prime Minister to delay the ban on new petrol and diesel cars caused the market to lose some value for the forward seasons and we also saw our first winter gale with Storm Agnes reaching land.

At the end of September, British gas storage was 97% full, with European storage at 95%. Levels are extremely comfortable as we approach winter, evidenced by the fact that there was a larger premium on pricing for winter 2024 than winter 2023.

The UK will not be complacent though; despite high gas storage levels, if we experience a cold winter this may drive prices upwards in quick succession.

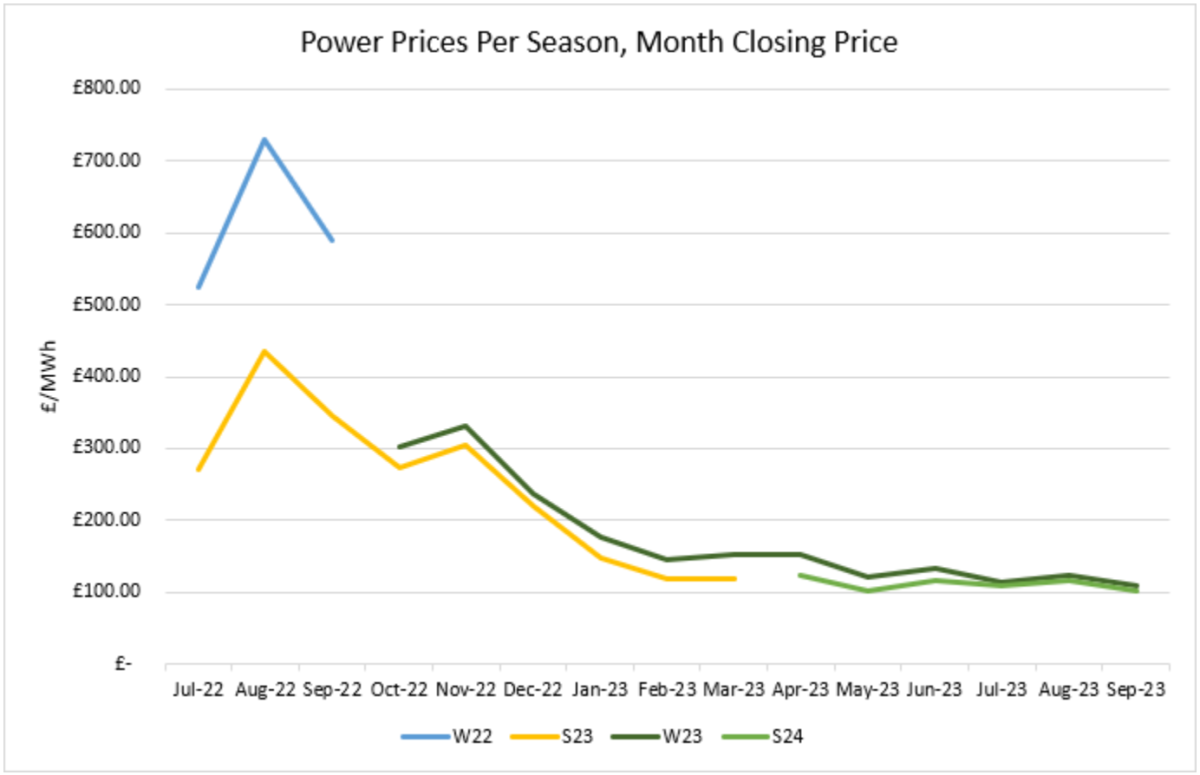

Prices ending in September hovered just above £100/MWh wholesale.

The Greenspan Agency produce the report on a best endeavours basis and has been supplied for your interest; the facts in this report are for background information and should not be relied upon exclusively for decision making.

If you have any queries about the content in this report, please contact amy@greenspanenergy.com or lara@greenspanenergy.com.

Contact Us

Send us a message

or enquiry

"*" indicates required fields