January has seen continued volatility in the gas and power markets, underpinned by fluctuating weather forecasts and renewable generation, keeping a tight supply/demand outlook. Cold temperatures and poor wind output early in the month saw increased pressure on gas for power demand and high withdrawals from storage. Pressure eased mid-month with milder temperatures along with wetter and windier conditions during Storm Éwoyn. Revised weather forecasts indicated below average temperatures for February, causing bullish movement amid concerns over replenishing gas storage at the end of the month. Geopolitical issues are ongoing with increased uncertainty for the markets. President Trump’s new energy policies, sanctions on Russia, and LNG supply levels, all keep the market highly sensitive.

Power

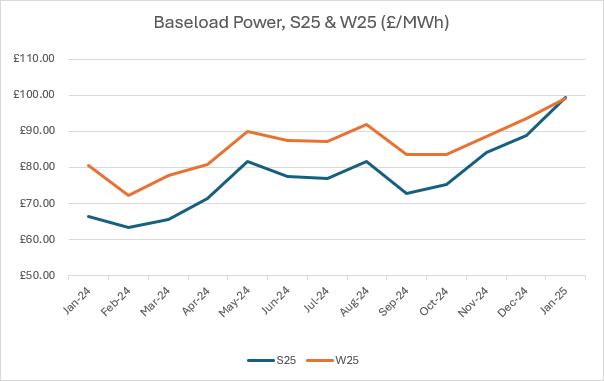

Seasonal contracts for baseload power were strong throughout January, slight dips during windier periods. Before gaining again, reaching their highest price in weeks. The S25 power contract traded at a premium to the W25 for the first time in several years, mirroring the continued growth in S25 gas contracts.

| Contract

(Baseload power) |

Closing Price, 31st January 2025 (£/MWh) | Month Movement |

| Summer 25 | £99.25 | +11.6% |

| Winter 25 | £99.02 | +7.2% |

Gas

Sustained gas for power demand throughout January as unchanged fundamentals kept the market tight. This winter premium is expected to continue into February as low temperatures are forecast across the UK and NW Europe, enhancing supply concerns. Gas markets continue to lift to compete with Asian markets for LNG cargoes. This effort to replenish storage will be a significant task, as levels sit at 27% in the UK. S25 contract continues to trade at a premium to W25, to sustain high LNG cargo imports. Twelve LNG cargoes expected over the next two weeks.

Looking ahead

Volatility is expected to continue across markets in February, as European weather, storage levels and geopolitical headlines drive demand upwards, with long term forecasts more uncertain. The outcome of tensions between Russia and Ukraine could impact prices. Further sanctions are imposed on Russia from the US and talks to restart gas transit through Ukraine are ongoing. Trump’s “Drill, baby, drill” sentiment suggests more US LNG supply to Europe, while US trade tariffs could also change global demand forecasts in the coming months.

The Greenspan Agency produce this report on a best endeavours basis, and it has been supplied for your interest; the facts in this report should not be relied upon for decision making. If you have any queries about the content in this report, please contact bureau@greenspanenergy.com

Contact Alba EnergyContact Us

Send us a message

or enquiry

"*" indicates required fields