October saw geopolitical tensions in the Middle East continue to underpin the market. Increased demand came with cooler temperatures at the start of the month. Light winds throughout late October supported the market although above average temperatures maintained a more bearish sentiment. Renewable generation accounting for 26% of the UK’s fuel generation on 31st October.

Power

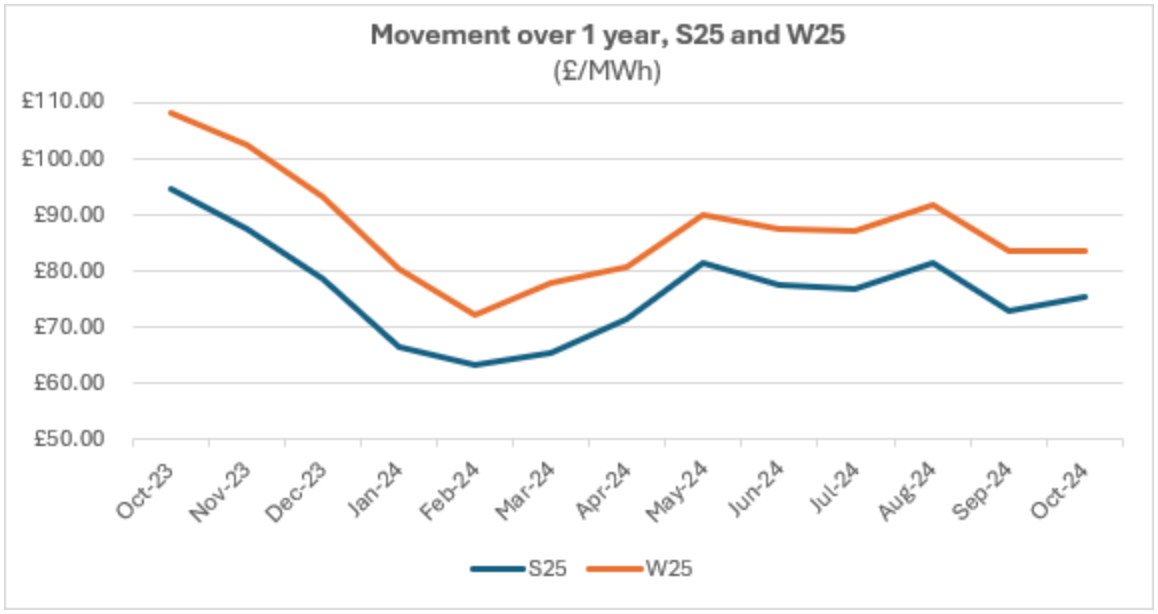

UK seasonal contracts reversed some of the previous session gains, with contracts remaining rangebound due to largely unchanged fundamentals.

REGO prices continue to soften, with CP24 (April 2025 to March 2026) trading at £4.40 /MWh last week for wind, solar and hydro.

| Contract | Closing Price, 31stOctober 2024 (/MWh) | Movement Over October |

| Summer 25 | £75.39 | + 2.1% |

| Winter 25 | £83.60 | -0.7 % |

Gas

Poor wind forecasts across the UK and NW Europe along with ongoing interconnector maintenance contributed to gas prices improving (6%) over October. Though strong UK gas storage, supported by EU import and LNG cargos, coupled with higher temperatures has weighed on contracts.

Looking ahead

As we move into the winter months, weather forecasts and gas flows will continue to drive the market. Continuing conflict in the Middle East could cause volatility and bullish development. A combination of these factors could disrupt supply and see short term gains for forward power prices, while robust gas supplies across Europe suggest a more bearish long-term outlook.

The Greenspan Agency produce this report on a best endeavours basis, and it has been supplied for your interest; the facts in this report should not be relied upon for decision making. If you have any queries about the content in this report, please contact bureau@greenspanenergy.com

Contact Alba EnergyContact Us

Send us a message

or enquiry

"*" indicates required fields