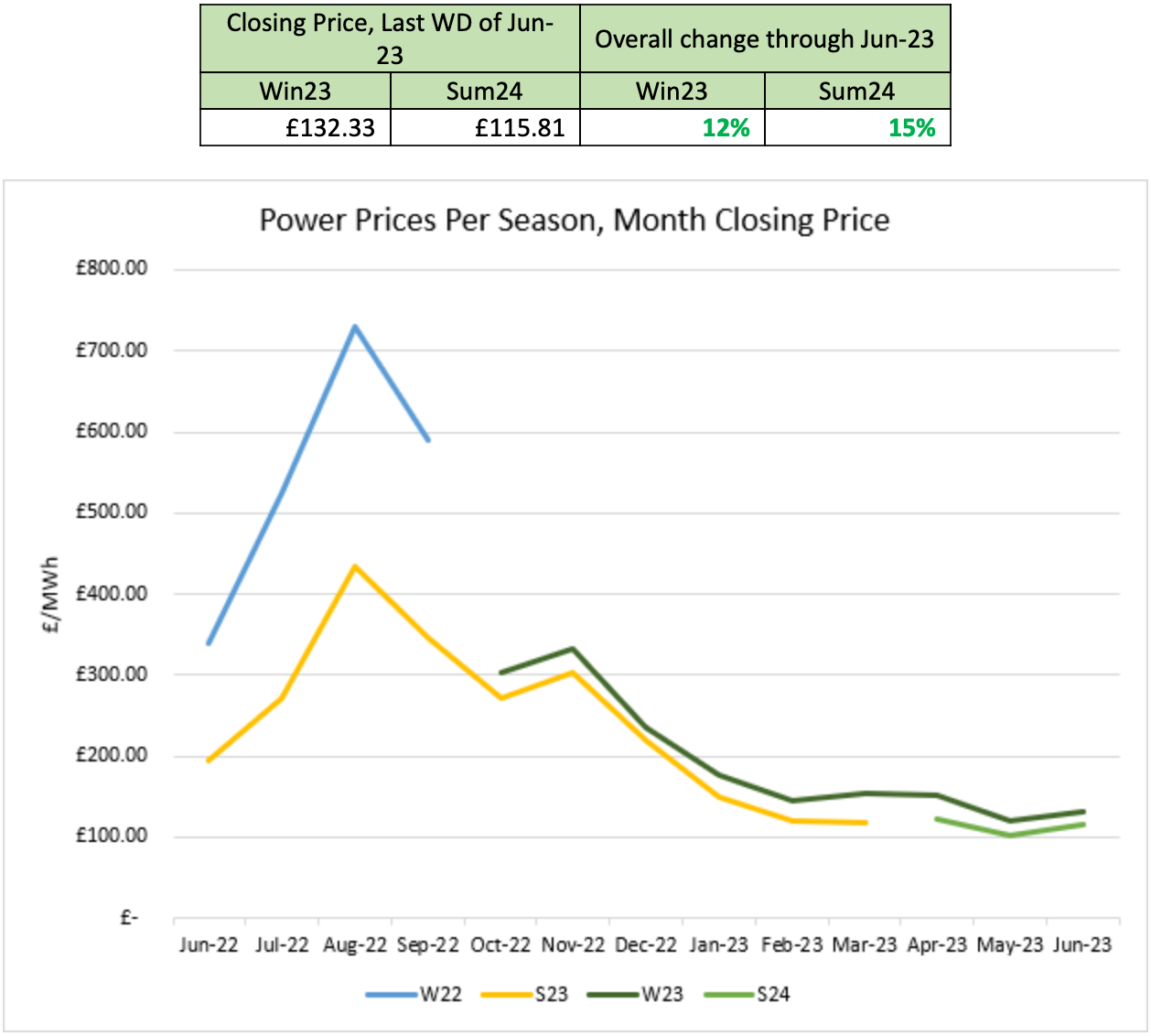

This month, we have witnessed the first substantial upward movement since 2023 began as Winter24 pricing rose by 12% and Summer24 rose by 15% within month. However, some volatility remained as varying solar and wind output influenced prices. Whilst European gas stocks remain high (at over 75% capacity, 20% more than this time last year), the decrease in LNG cargoes sent to the UK has impacted pricing. The fate of European gas supply ahead of the upcoming winter season seems to remain a significant market pressure.

The start of June saw solar generation exceeding seasonal norms by 20%, bolstering renewable generation despite the low wind outputs. Summer24 pricing started the month <£100/MWh mark.

Towards the end of the first week, it became apparent that LNG supplies would remain low throughout the month. Furthermore, CCGT availability decreased considerably compared to this time last year. Gas and power prices rose to attract LNG to the UK, as the market felt pressure to meet storage demand well in advance of the upcoming winter.

Rising prices continued into the mid-month; Norwegian gas outages were announced at the Troll gas field, among others. This was coupled with low wind output, bolstering prices further.

Stormy weather caused an increase in wind generation in the final week of the month, reducing the pressure from low LNG and gas deliveries to the UK. Overall, there was a 20% drop in LNG cargo deliveries to the UK in June as the UK was outbid by other markets.

The impact of the Russian Mercenary revolt was seen mainly on oil pricing. With Europe now sourcing gas from the US and other suppliers, the power market seems to be somewhat protected from the influence of developments within the Ukrainian war at this point in time.

The Greenspan Agency produce the report on a best endeavours basis and has been supplied for your interest; the facts in this report are for background information and should not be relied upon exclusively for decision making.

If you have any queries about the content in this report, please contact amy@greenspanenergy.com or lara@greenspanenergy.com.

Contact Us

Send us a message

or enquiry

"*" indicates required fields