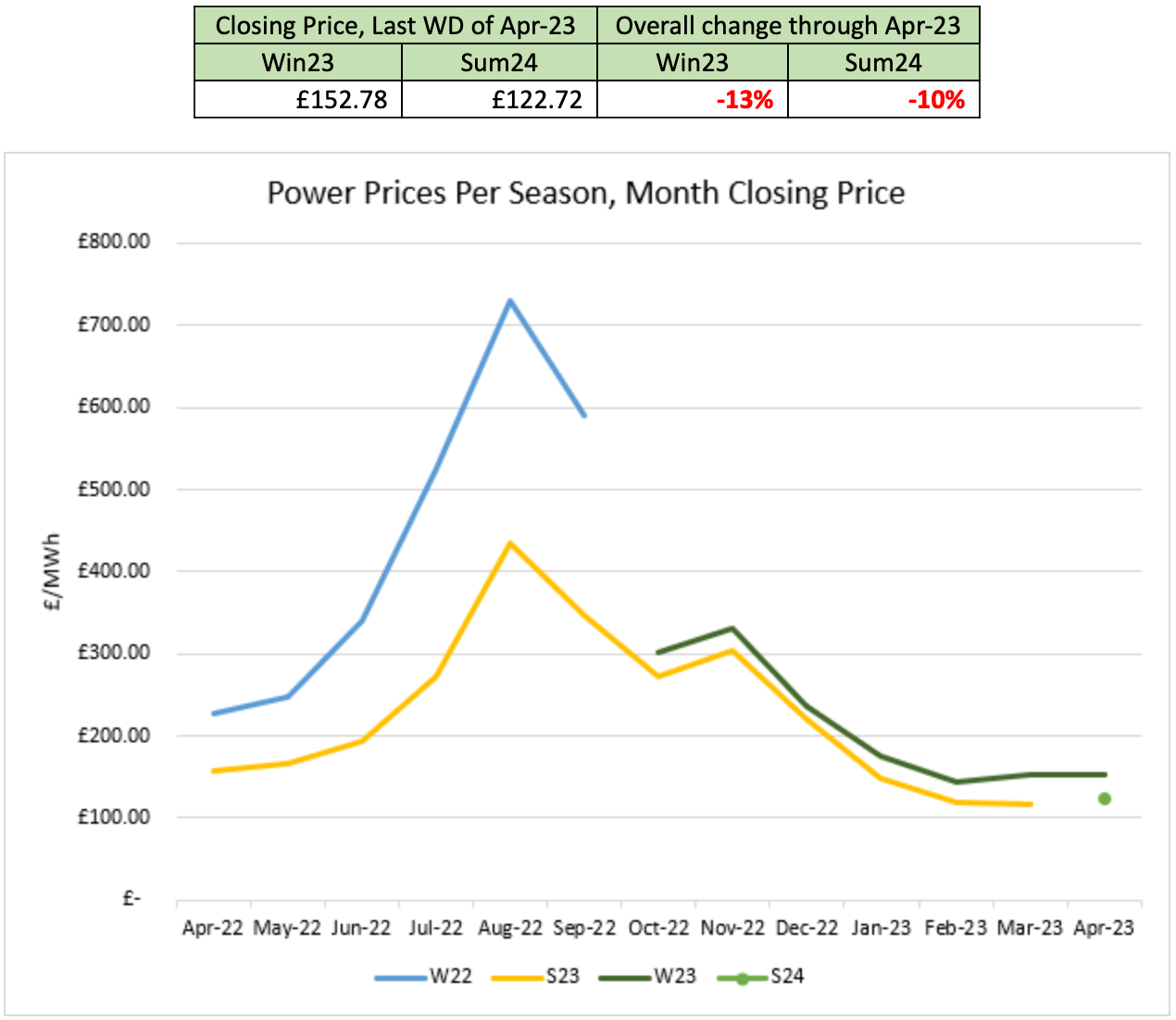

April gifted the UK with the arrival of spring and a welcome increase in temperatures. This, amongst other market drivers, saw further decreases in seasonal pricing, despite concerns around French Nuclear availability and Norwegian gas outages. Decreases were partially driven by record LNG supply to Europe; European LNG pricing sits at a premium to the Asian market as China’s LNG demand remains 11% below historic norms. Overall, Winter23 pricing decreased by 13% from month open to month close, whereas Summer24 decreased by 10%.

Cold weather at the start of the month contributed to increases in gas prices (and subsequently power). This was further bolstered by continuing strikes in France. However, price rises were short lived as weather fundamentals (temperature and wind output) were revised upwards for the remainder of the week.

Whilst uncertainty over French power availability persisted through to the middle of the month, this was met with high winds and strong LNG supply. Despite the loosening of COVID restrictions in China, the LNG demand for the country remains lower than historic levels and Europe remains the premium market.

Overall, the electricity market continued its downward trajectory. Trading became rangebound due to the aforementioned opposing market pressures. As the month came to a close, further concerns around Norwegian gas field outages caused minor market increases, but these failed to recoup losses seen earlier in the month.

In general, risk remains over both power and gas supply in the further terms. The IEA recently stated that Russian oil exports have now rebounded to levels last seen pre-April2020 (although prices remain heavily discounted). Furthermore, OPEC+ announced cuts to supply to manage price decreases, despite push back from large consumers such as the US. This is likely to further impact apparent demand destruction and decreases in global industrial activity.

With the strong LNG supply and demand decreases seen this winter, European gas levels remain at 55% in April; well above the 5-year average. Less injection demand will be needed to reach the “90% full target” by the coming winter, but summer temperatures and the ongoing war in Ukraine ensures that uncertainty remains.

The Greenspan Agency produce the report on a best endeavours basis and has been supplied for your interest; the facts in this report are for background information and should not be relied upon exclusively for decision making.

If you have any queries about the content in this report, please contact amy@greenspanenergy.com or lara@greenspanenergy.com.

Contact Us

Send us a message

or enquiry

"*" indicates required fields