Back in November 2021, power prices were looking turbulent. Little did anyone know just how volatile they were going to become. Power prices were that were hitting highs of £250/MWh towards the end of 2021 had become £500/MWh at the start of 2022.

Whether by chance or design, Russian flows to Europe remained low throughout the end of 2021 and Asia consistently outbid Europe for Liquefied Natural Gas (LNG).

Over 30 energy suppliers exited the market, as poor credit and hedging strategies failed to soften the impact of the extreme volatility.

Whilst the market settled slightly in January following a mild winter and increased LNG deliveries to Europe, the Russian Invasion of Ukraine in late February pushed the market into a frenzy.

Annually the UK receives around 4% of its natural gas from Russia. However due to our low storage capacity, the UK market is strongly linked to the European market and storage capacity. European sanctions on Russian gas ultimately feed through into UK prices.

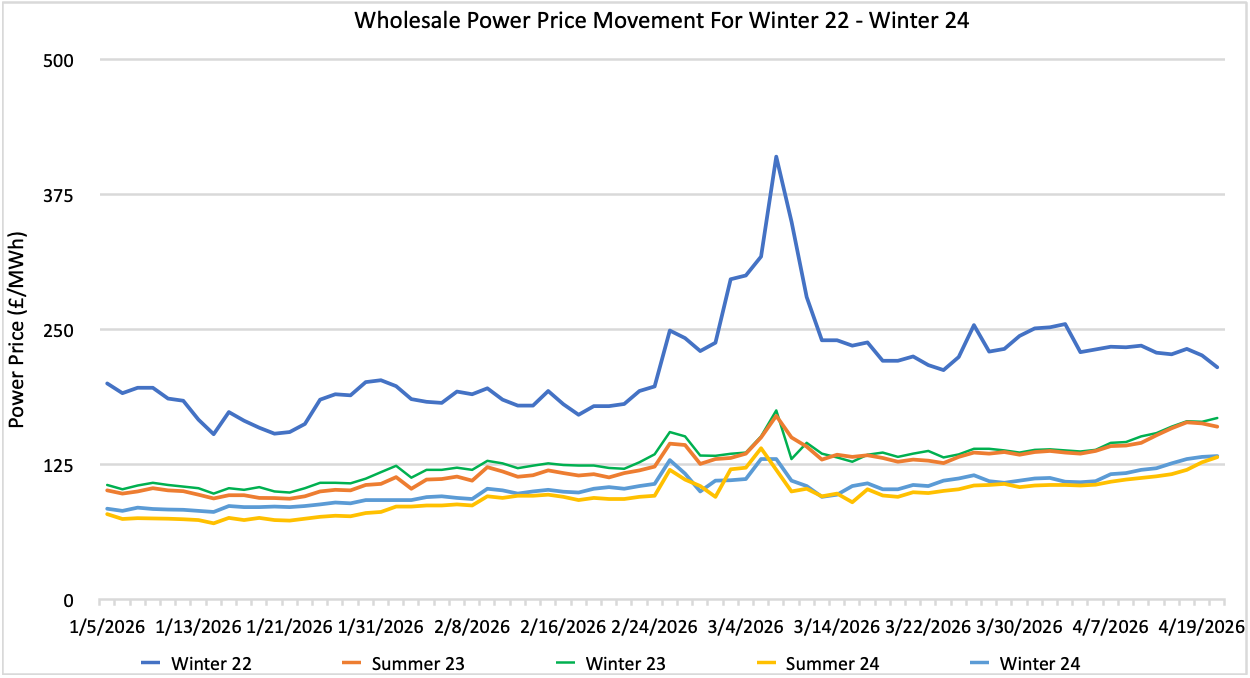

Figure 1: Wholesale Power Price Movement for Winter22-Winter24.

Risk, Balance, and the Luxury of Hindsight

This begs the question, are high prices (and increased market volatility) the new normal, or will we return back to the pre-pandemic scenario if the war ends? Without a crystal ball, we can’t be sure. The nature of the electricity market has always left generators and suppliers open to risk. For now, power prices are high, and many generators will be able to secure Power Purchase Agreements (PPAs) at rates far higher than previously obtained.

Yet, given the low renewable output of 2020 and 2021, coupled with European sanctions on Russian commodities (coal and oil, as well as gas), fears over insufficient electricity supply may continue to feed into the market, and inflate prices.

What’s Next?

Over the summer, the UK Government responded to new market conditions by emphasising the need for increased “home grown” energy supply. Reducing our reliance on foreign fossil fuel markets (i.e., Russian gas) takes precedence even over net zero. As export power prices increased do did bills for business consumers.

But onsite renewable generation, especially for industrial consumers, can mitigate the impact of rising electricity bills.

With the increased risk, our advice continues to be that the creditworthiness of your counterparty remains paramount when negotiating PPAs or import agreements. A reputable broker will help to cut through the noise of price drivers, and present opportunities as they arise in an increasingly volatile market.

August 2022

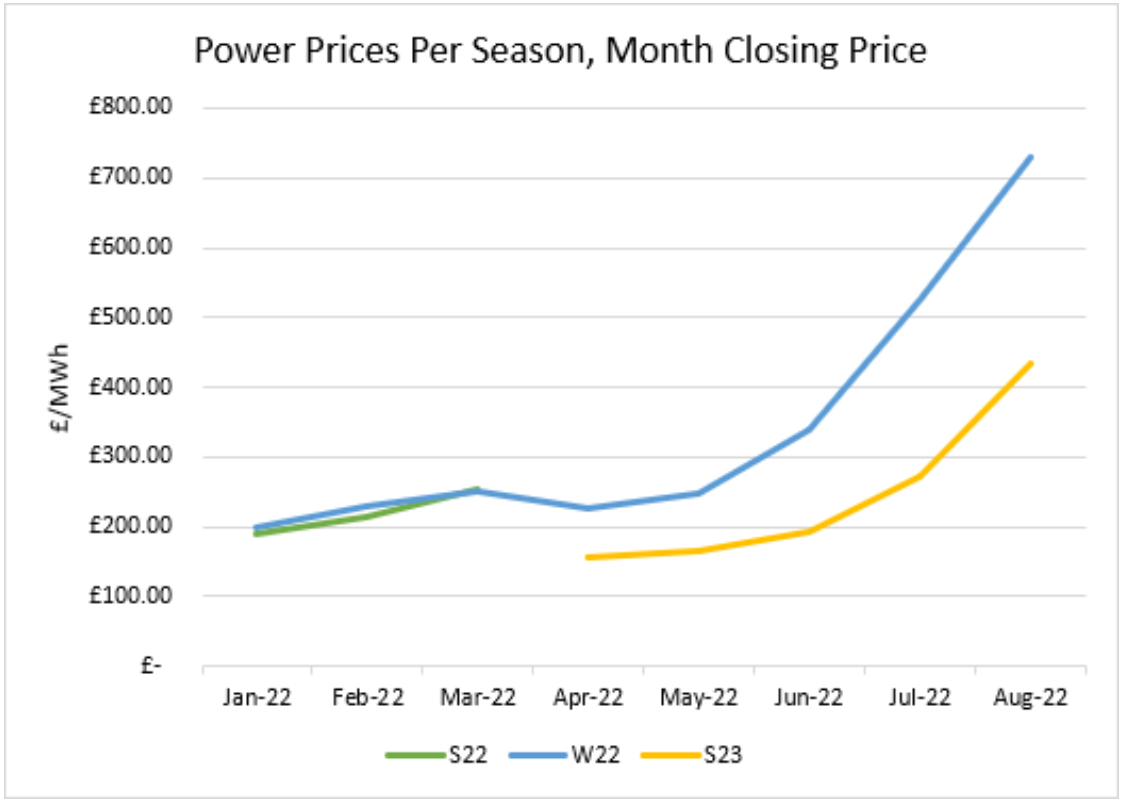

August saw another month of power increases across all terms, with Winter 22 increasing by 27%, and Summer 23 increasing by a shocking 36%.

Power prices seemed to be falling at the start of August; with Norwegian gas supporting Russian flows, the overall picture for the month was sustained increase across the board. Heightened fears for Winter gas supply (and therefore power) remained a key market driver.

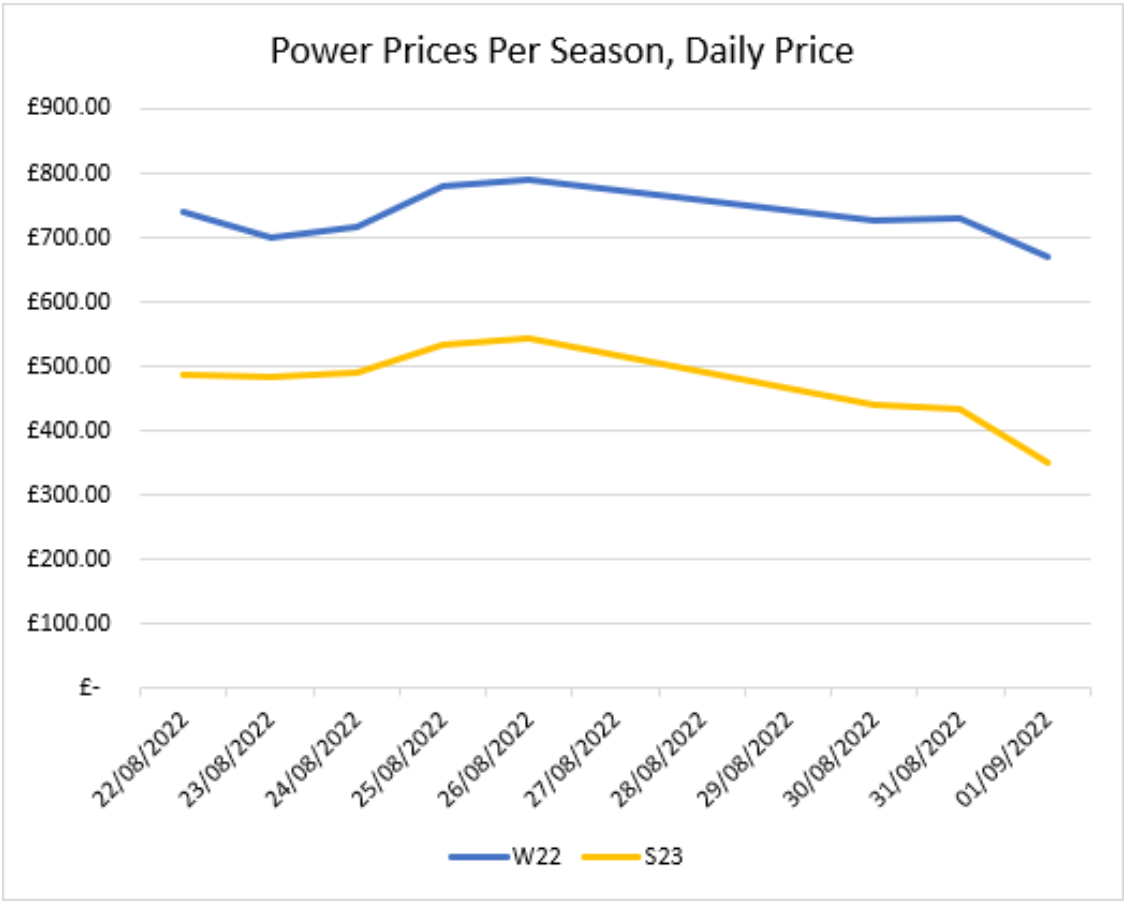

The second half of the month was influenced by Norwegian outages and limited US LNG supply shortages. Whilst Russian supplies have largely remained consistent (albeit low); fear and uncertainty that these gas supplies will be cut continued to weigh heavily on the market. Prices rose astronomically as the month went on, peaking on 26/08/2022.

The news in late August that the EU were considering intervening with gas prices caused tremors in the market. Drops of c.a. £150/MWh were seen before the month closed (see the second graph in this report).

Last week, scheduled maintenance on Nordstream 1 occurred as expected and flows were expected to resume following the brief downtime. But this remains uncertain.

Market movement for the last fortnight:

The Greenspan Agency produce the report on a best endeavours basis and has been supplied for your interest; the facts in this report are for background information and should not be relied upon exclusively for decision making.

If you have any queries about the content in this report, please contact amy@greenspanenergy.com or lara@greenspanenergy.com.