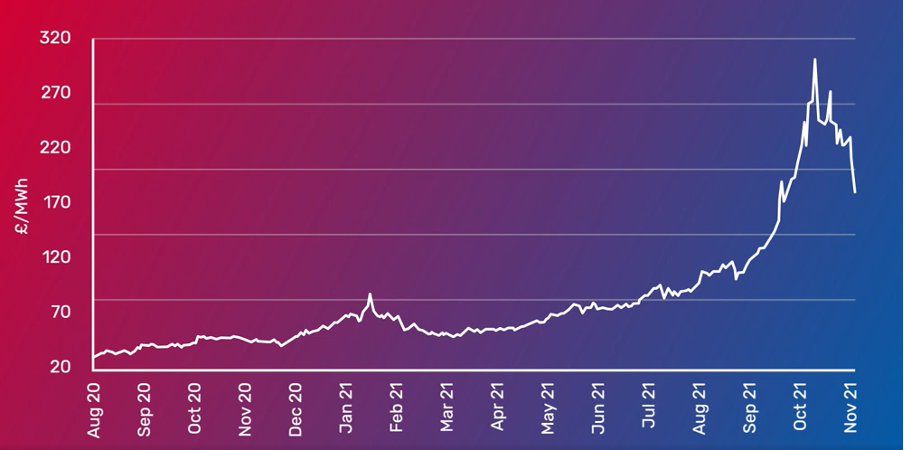

As many renewable generators are well aware, it has been a turbulent few years in the electricity market. Great Britain has entered the Winter 2021 season with record high electricity prices at £250/MWh. A far cry from the extreme low prices of Summer 2020 of £24/MWh.

The Electricity Market: Past, Present and Future

The Past

The effect of COVID-19 on the world market was unprecedented; global lockdowns brought many businesses to a standstill, resulting in a huge drop (65% or higher) in commodity demand. Electricity prices remained low and dependent on oil and gas markets throughout Summer20, despite the lifting of COVID restrictions worldwide.

As we moved into Winter20, many countries re-entered lockdown as COVID-19 cases soared. The northern hemisphere also experienced a La Niña event, bringing a cold winter to key markets (China and Europe especially). This was coupled with unseasonably low renewable output throughout the UK and Europe. A global trade war on gas and LNG began; with China dominating LNG demand and Russia restricting gas flows, Europe was forced to rely heavily on its existing gas storage.

Summer21 began with European gas storage levels 10% lower than the 10-year average, which unfortunately was met with a global increase in gas demand as the world moved out of lockdown. Renewable output, however, remained well below seasonal normal, and reliance on gas for electricity production remained. High gas demand was met with low gas supply as flows from Russia were continually constrained throughout the summer; it is likely that flows will remain low until the commissioning delays for the new Russia-Europe gas pipeline (Nord Stream 2) are dealt with.

Figure 1: Electricity Prices for Month Ahead Contract

The Present

European gas storage capacity is at a measly 75% heading into winter. Gas supply remains tight and uncertain, and Russia continues to prioritise domestic supply over European export. China dominates LNG trades in an attempt to maintain their own storage, pricing Europe out of key marginal commodities.

Although October brought higher wind and hydro output, this increase in renewable generation failed to significantly reduce gas demand or electricity prices. As the volatility in the market remains, suppliers continue to take a risk averse approach to power purchase agreements (PPAs). Smaller, less credit worthy suppliers have stepped back from offering fixed PPAs to small-medium renewable generators amid uncertainty on output. Lack of creditworthy tendering parties has reduced competition on PPA pricing. The bigger suppliers are constantly reviewing and changing their pricing strategies as the markets fluctuate. That being said, prices remain almost double the guaranteed FiT Export Tariff rate, which is currently at £56.50/MWh, out to Mar23.

The Future

National Grid have estimated that the baseload capacity in Great Britain is sufficient to meet demand throughout winter and beyond. However, uncertainty and caution in the market remains. The baseload mix in Great Britain is now heavily reliant on variable generation (wind and solar) and thus volatility in the market is expected to become a more permanent feature. Weather patterns suggest that the global north is likely to experience another La Niña event this coming winter and cold weather may be on the horizon. Electricity prices are expected to remain closely tied to the increasingly volatile gas market for the coming months.

Be Prepared

The last two years have been a rollercoaster for the energy sector, swinging from the lowest to the highest power prices in the space of 12 months. Backwardation in the electricity market suggests that the extreme high prices are to be short lived, but uncertainty remains.

At the time of writing 17 energy suppliers have collapsed in the last two months. Ensuring your counterparty is credit worthy remains paramount for protecting your revenue in an increasingly volatile market.

The factors driving price movement remain complex; seeking the advice of a worthy broker to cut through the noise can be invaluable. It is important to be ready and poised to take advantage of the opportunities in this volatile and uncertain climate.

Contact Us

Send us a message

or enquiry

"*" indicates required fields