The UK gas and power markets were primarily influenced by the progress of the ceasefire negotiations between Ukraine and Russia. With no official agreement reached yet, the markets remained sensitive to the ongoing discussions, many of which were heavily influenced by President Trump.

Mild weather and stable fundamentals kept the downward trend into early March. However, attacks on Ukrainian gas infrastructure and a cooler spell prompted some bullish movement in the markets, though any volatility was brief, and contracts traded within range. As March came to a close, the markets softened with the arrival of warmer temperatures and increased wind and solar generation, signalling the end of the winter season.

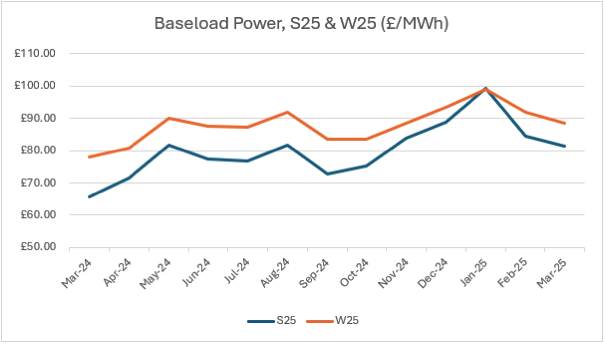

Power

Seasonal contracts for baseload power experienced some short-term volatility but have closed with little movement since February, with both Summer25 and Winter25 trading at lower levels.

This marks the conclusion of the Summer25 contracts, and focus turns to Winter25 and Summer26 contracts.

REGO markets continued to fall, trading at £1.50/MWh for wind, solar and hydro (CP24).

| Contract

(Baseload power) |

Closing Price, 31st March 2025 (/MWh) | Month Movement |

| Summer25 | £81.57 | -3.76% |

| Winter25 | £89.67 | -2.44% |

Movement over 1 year, S25 and W25

Gas

There has been a decrease in gas-for-power demand and fewer storage withdrawals. Coupled with robust LNG cargo supply from the U.S. has seen the supply outlook stabilised and has allowed for storage injections in Europe. A further bearish sentiment in the gas market where winter risks are lessened and cooling demand for summer hasn’t yet begun. Additionally, ongoing discussions about future European storage targets, lobbyists suggest lowering the targets could help ease supply pressure and minimise volatility in the gas market going into Winter.

Looking ahead

Market attention will continue to be on the outcome of the Ukraine-Russia ceasefire, and the question of whether Russian gas will return to Europe remains unresolved. The U.S. continues to impose and threaten tariffs, which are influencing growth factors for many countries and altering demand projections. As we enter the summer season, the focus will shift to replenishing depleted storage, and we can expect less volatility in both the gas and power markets.

FiT and ROC Rates: April 2025 – March 2026

Please note that Ofgem have confirmed the FIT RPI increase for Apr25 is 3.5%.

The ROC Buyout price for 2025-26 has been published by Ofgem at £67.06/ROC.

The Greenspan Agency produce this report on a best endeavours basis, and it has been supplied for your interest; the facts in this report should not be relied upon for decision making. If you have any queries about the content in this report, please contact bureau@greenspanenergy.com

Contact Alba EnergyContact Us

Send us a message

or enquiry

"*" indicates required fields